AI-driven AML transaction monitoring has become the answer to the current issues with monitoring AML transaction as traditional rule-based monitoring is failing banks. Criminals adapt faster than static rules can keep up, false positives drown investigation teams, and regulators are losing patience.

This article covers what’s driving the shift, what regulators expect, and how banks can implement AI monitoring without falling into the most common traps.

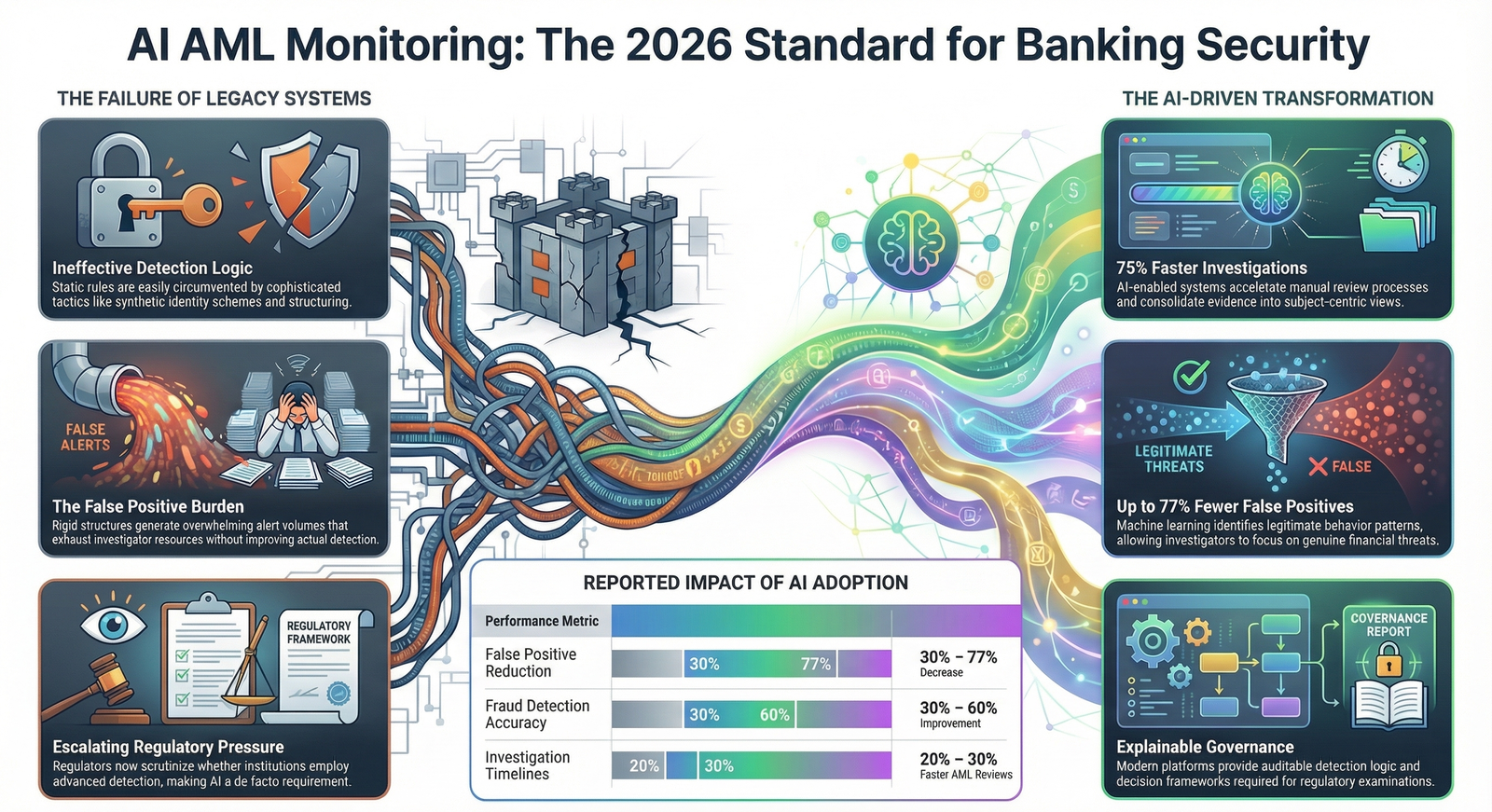

Why Rule-Based Systems Stopped Working

Legacy transaction monitoring created two problems that regulators could no longer tolerate:

- Detection gaps. Rigid rules missed sophisticated laundering techniques like structuring across multiple accounts, rapid cross-border transfers, and synthetic identity schemes.

- Alert overload. Systems generated massive volumes of false positives that buried investigators in irrelevant work while real threats slipped through.

As transaction volumes exploded across digital channels, manual review became physically impossible. Banks were forced to choose between alert fatigue and compliance gaps. Neither option satisfied regulators, and enforcement actions followed.

What Regulators Now Expect

Global regulators including FATF, FinCEN, and national authorities across APAC and Europe have moved beyond requiring basic monitoring. The current expectation is:

- Continuous adaptation to new money laundering typologies and terrorist financing methods

- Comprehensive audit trails with clear, explainable detection logic

- Advanced detection capabilities that exceed minimum regulatory thresholds

- Regular model performance reviews, bias testing, and false positive tracking

AI adoption is no longer a competitive advantage. It is a de facto regulatory requirement. Enforcement agencies increasingly penalize institutions that rely solely on legacy systems when proven AI alternatives exist.

Regulatory examinations now include detailed reviews of AI model governance, and banks that cannot demonstrate how their systems make detection decisions face direct enforcement risk.

The Business Impact: By the Numbers

Banks deploying AI-driven monitoring are reporting measurable results:

- 20 to 30% faster AML investigations

- 30 to 40% faster profiling and detection

- 30 to 77% reduction in false positives depending on implementation maturity

- 60% improvement in detection accuracy at institutions like DBS Bank

- 75% faster investigation completion compared to manual review

- ~€3.5 million in annual savings at one European bank through improved case management

For customers, the benefit is twofold: better fraud protection and fewer false blocks on legitimate transactions.

For compliance teams, the shift creates new accountability. Regulators now demand explainable AI logic and audit-ready decision frameworks, moving responsibility from rule interpretation to model validation and continuous performance monitoring.

How AI Transaction Monitoring Actually Works

AI systems build behavioral baselines by training on historical transaction data, learning what normal activity looks like for each customer segment and account type. Instead of triggering on fixed thresholds, they flag deviations from established patterns.

The most effective implementations layer multiple detection signals:

- Transaction patterns. Volume, frequency, amounts, and counterparty relationships

- Device intelligence. Login behavior, device fingerprints, and session anomalies

- Behavioral analytics. Spending habits, channel usage, and timing patterns

- Geolocation analysis. Transaction origins compared to customer history and risk profiles

This multi-signal approach catches coordinated attacks and sophisticated schemes that single-rule systems miss entirely.

What a Strong Implementation Looks Like

Technical Foundation

- Real-time processing that evaluates transactions as they occur, not in overnight batches

- Integration of KYC and customer due diligence data with transaction monitoring for contextual risk scoring

- ML models trained specifically to detect structuring, cross-border laundering, and high-risk jurisdiction activity

- Automated SAR generation that compiles evidence and populates regulatory templates

Governance Framework

- Clear ownership and accountability for AI model performance

- Automated testing protocols to catch bias and performance degradation

- Comprehensive audit logs covering every detection decision and investigator action

- Regular stress testing against emerging financial crime typologies

- Documented incident response procedures for model failures

Continuous Improvement

- Quarterly model performance reviews against baseline metrics and industry benchmarks

- Feedback loops where investigation outcomes inform model retraining

- Systematic tracking of emerging crime methods to update detection capabilities

- Active engagement with regulators to stay aligned with evolving expectations

- Participation in industry information-sharing forums

Common Mistakes That Undermine AI Monitoring

Even well-funded implementations fail when banks make these errors:

- No governance framework. Deploying AI without explainability creates black-box detection that regulators will reject during examinations.

- Skipping behavioral baselines. Without proper baseline training, models generate excessive false positives that erode investigator confidence.

- Bad underlying data. Layering AI on top of legacy systems with poor data quality limits model effectiveness and creates new compliance gaps.

- No retraining process. Models degrade as fraud tactics evolve. Without continuous monitoring and retraining, detection accuracy drops over time.

- Treating it as a tech project. AI implementation is a compliance transformation. Banks that don’t redesign investigation workflows and case management alongside the technology capture only a fraction of the potential efficiency gains.

Where the Industry Is Headed

47% of businesses now use AI-based tools for fraud detection, making it the most common AI application in payments. Major institutions including DBS Bank, Absa, and leading European banks have already replaced legacy systems with AI-powered platforms.

Technology vendors are consolidating transaction monitoring, customer due diligence, sanctions screening, and case management into unified platforms with explainable AI and audit-ready workflows. This consolidation reflects the reality that fragmented systems cannot meet current regulatory expectations.

The trajectory is clear: banks that embrace AI-driven monitoring will strengthen their compliance posture and reduce costs. Those still running legacy systems face growing enforcement exposure, competitive disadvantage, and the risk of missing financial crimes that their peers would have caught.

Frequently Asked Questions

How much can AI improve fraud detection accuracy?

Banks report improvements ranging from 30 to 60%, with top performers like DBS Bank achieving 60% better detection accuracy. False positive reductions of 30 to 77% free investigators to focus on genuine threats.

How does AI reduce false positives?

AI models learn normal behavior patterns for each customer and account type from historical data. Rather than triggering on static thresholds, they flag meaningful deviations from established baselines, dramatically improving the signal-to-noise ratio.

What regulatory requirements drive AI adoption?

FATF, FinCEN, and national regulators require suspicious pattern detection, SAR filing, and comprehensive audit trails. The growing expectation for advanced detection capabilities that exceed minimum thresholds has made AI a practical compliance necessity.

What governance is required for AI monitoring systems?

Banks need clear model ownership, automated bias and performance testing, comprehensive audit logs, regular stress testing against emerging crime types, and documented incident response procedures. Explainable AI logic is now a regulatory expectation, not a nice-to-have.

How should banks approach implementation?

Start with a gap assessment of existing infrastructure. Prioritize real-time monitoring, integrate KYC data with transaction systems, establish behavioral baselines, and build case management that consolidates alerts into subject-centric views. Governance and feedback loops should be designed alongside the technology, not added afterward.

One thought on “AI AML Monitoring: Banks’ 22% Fraud Shield in 2026”