It is observed in financial services industry there is frequent change in rule. Banks spend months building a program around one set of rules, and then the ground shifts. New guidance drops. A regulator changes priorities. A political transition rewrites the playbook overnight. By 2026, this cycle has a name that most compliance professionals use with a grimace: regulatory whiplash.

But some banks absorb these shocks and keep moving. Others scramble, bleed money, and end up on the wrong side of an enforcement action. The difference is not luck. It comes down to how institutions build their compliance foundations, how they use technology, and whether they treat regulatory change as a crisis or simply as the cost of doing business.

This article breaks down what actually shields financial institutions from regulatory whiplash, with real numbers, practical frameworks, and hard lessons from the institutions that got it right and those that did not.

The Regulatory Maze Banks Are Navigating Right Now

The sheer volume of rules that financial institutions must follow in 2026 is staggering. Banks are simultaneously answering to frameworks including the Bank Secrecy Act, MiFID II, GDPR, SEC rules, FINRA standards, and the Anti-Money Laundering Act. Each of these carries its own reporting obligations, customer due diligence requirements, suspicious activity filing mandates, and record-keeping standards.

And the regulators behind these rules are not sitting idle. The Financial Conduct Authority in the UK, the Office of the Comptroller of the Currency, the FDIC, and the Financial Intelligence Centre are all pushing harder for transparency, faster reporting, and tighter controls. The SEC alone launched 200 enforcement actions in Q1 2025, sending a clear message that regulators are not waiting for banks to catch up.

The complexity multiplies for institutions operating across borders. A bank headquartered in New York with operations in London and Singapore is not just following one set of rules. It is reconciling overlapping and sometimes contradictory requirements from multiple jurisdictions at the same time. MiFID II demands accurate transaction reporting in Europe, and failures in that area have already resulted in multimillion-dollar fines for major banks like UBS and Barclays. Meanwhile, GDPR adds data privacy obligations that can conflict with the transparency requirements of financial regulators.

This is not a theoretical problem. It is the daily reality for compliance teams in 2026.

Why Regulatory Whiplash Hit So Hard

Regulatory whiplash did not appear out of nowhere. It built up over years of political shifts, economic instability, and high-profile institutional failures that forced regulators to react aggressively.

When seven major banks were caught with serious MiFID reporting lapses, regulators responded with stricter enforcement across the board. When pandemic-era economic interventions created new financial crime vulnerabilities, AML requirements tightened. When geopolitical tensions escalated, sanctions regimes expanded faster than most compliance teams could track.

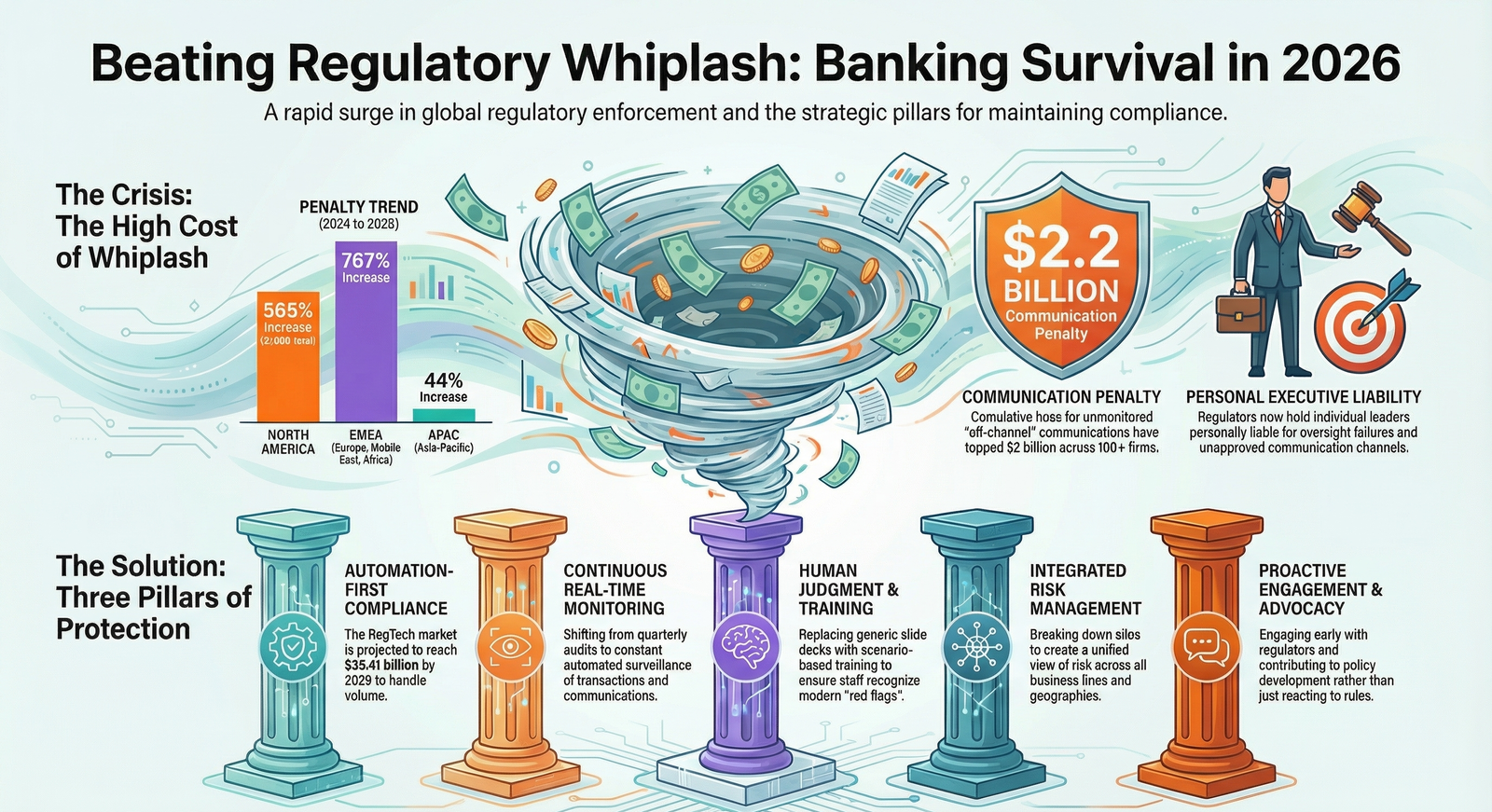

The numbers tell the story clearly. Global regulatory fines issued to financial institutions in the first half of 2025 totaled $1.23 billion, representing a 417% increase compared to the same period in 2024, when 118 fines totaled just $238.6 million. Penalties from North American regulators alone surged 565% to over $1.06 billion.

And while full-year 2025 figures showed some moderation in the global total, the regional picture remained volatile. Total penalties for AML, KYC, sanctions, and customer due diligence violations reached $3.8 billion in 2025, down from $4.6 billion in 2024. But that decline was driven almost entirely by a drop in North American fines. Penalties in EMEA surged 767% and APAC fines rose 44%, showing that enforcement pressure is not easing but shifting geographically.

This moment matters because 2026 thresholds are amplifying scrutiny on risk management, transparency, and the speed at which institutions can respond to new requirements. Banks that were already stretched thin are now being asked to do more, faster, with higher stakes for getting it wrong.

The Real Cost of Getting It Wrong

The financial consequences of non-compliance have moved well beyond the “cost of doing business” category. Cumulative fines for unmonitored communications alone have now topped $2 billion, with over 100 firms penalized specifically for off-channel communication failures totaling $2.2 billion.

But fines are just the beginning. Non-compliance triggers a cascade of damage that includes license risks, operational disruptions, reputational harm, and personal liability for the individuals responsible for oversight failures. Boards are now requiring trend reporting on emerging regulatory threats, and decision-making across institutions has shifted toward risk-prioritized strategies that put compliance at the center of business planning rather than treating it as an afterthought.

Regulators have also begun holding individual executives personally liable for conducting business on unapproved channels, often resulting in personal fines or suspensions. This is not an abstract threat. It means that the compliance officer, the managing director, and the head of trading all carry personal exposure when their teams cut corners.

The reputational dimension is equally punishing. Unlike typical settlements where a firm neither admits nor denies wrongdoing, the SEC has increasingly required public admissions of record-keeping failures, creating lasting damage that follows an institution far beyond the initial penalty.

What Actually Protects Banks: The Five Pillars

After studying the institutions that weather regulatory whiplash most effectively, a clear pattern emerges. Protection does not come from any single tool or policy. It comes from layering five core capabilities that work together.

1. Build a Compliance Program That Bends Without Breaking

The banks that survive regulatory whiplash are not the ones with the thickest policy manuals. They are the ones with programs designed to absorb change. That means starting with a structured foundation that includes employee training on ethics, risk identification, and regulatory obligations tailored to the specific products, customers, and jurisdictions each team handles.

Regular risk assessments are essential, not as annual checkbox exercises but as living processes that reprioritize based on real-world signals. Credit risk, operational risk, liquidity risk, and emerging threats like AI-related compliance obligations all need to be evaluated on a rolling basis.

Dedicated compliance officers with genuine authority and visibility into business operations make this possible. When compliance lives in a silo with no seat at the table during business decisions, gaps form quickly and quietly.

2. Let Technology Do the Heavy Lifting

This is where the data becomes impossible to ignore. The global RegTech market is projected to expand from $13.18 billion in 2023 to $35.41 billion by 2029, and that growth reflects a fundamental shift in how banks approach compliance. Manual processes simply cannot keep pace with the volume and velocity of regulatory change in 2026.

According to Bain and Company, 15 to 20% of banks’ operational expenses are already allocated to governance, risk, and compliance. PwC highlights that companies spend between $1 million and $5 million on compliance for every $1 billion in revenue. Those numbers are only sustainable if technology is doing the repetitive, high-volume work that used to require armies of analysts.

Unified platforms that provide real-time regulatory updates, automated workflows, and AI-driven risk insights are no longer luxuries reserved for the largest global banks. RegTech-as-a-Service models now offer cloud-based solutions that scale for community banks and mid-tier institutions, making sophisticated compliance automation accessible without massive upfront infrastructure investment.

By 2026, 26% of digital onboarding processes in banking are expected to use AI, up from just 8% four years ago. That shift toward AI-powered KYC, transaction monitoring, and regulatory change tracking is transforming compliance from a reactive function into a predictive one.

The practical applications matter most here. Horizon scanning tools that alert compliance teams to regulatory changes before they take effect. Automated impact assessments that map new rules to existing controls and flag gaps immediately. AI-driven transaction monitoring that reduces false positives while catching genuine suspicious activity faster than any human team could manage alone.

3. Make Continuous Monitoring Your Default Setting

The days when banks had weeks to compile reports for regulators are over. Oversight bodies now expect data in days, sometimes even hours, and systems built for a slower era simply cannot keep up.

Continuous monitoring means exactly what it sounds like. Real-time tracking of transactions, communications, third-party risk, and regulatory developments. Not quarterly reviews. Not annual audits followed by months of remediation. Constant, automated surveillance with human judgment applied where it matters most.

This includes centralizing third-party risk management so that vendors, partners, and service providers are continuously evaluated for compliance, cyber, and financial risks rather than checked once during onboarding and forgotten. It means tracking regulatory updates as they happen and feeding them directly into policy management systems so that the gap between a new rule being published and your controls being updated shrinks from months to days.

4. Train People Like Compliance Depends on Them (Because It Does)

Technology handles volume. People handle judgment. And no compliance program survives regulatory whiplash without employees who understand not just what the rules say but why they exist and how to apply them when situations get ambiguous.

Effective training in 2026 goes beyond annual slide decks and checkbox certifications. It means plain-language explanations of complex rules. It means scenario-based exercises that reflect real situations teams encounter in their specific roles. It means integrating compliance training into the daily workflow rather than treating it as a separate obligation that competes with “real” work.

Staff across the organization need to understand BSA record-keeping requirements, AML duties, KYC obligations, and the specific risks associated with their products and customer base. When an employee in a branch office or on a trading desk recognizes a red flag and escalates it correctly, that is the compliance program working. When they do not, all the technology in the world will not save you from the enforcement action that follows.

5. Audit Relentlessly and Actually Fix What You Find

Routine internal audits serve three critical functions. They detect gaps before regulators do. They create a documented trail of proactive risk management. And they build the exam-ready documentation that proves to regulators your institution takes compliance seriously.

But auditing without remediation is theater. The banks that protect themselves from regulatory whiplash are the ones that close the loop. They identify findings, assign ownership, set deadlines, track progress, and verify that fixes actually work. They establish feedback loops from audits, regulatory exams, and market signals that continuously refine the compliance framework rather than letting it calcify between review cycles.

How the Smart Banks Are Responding Right Now

The enforcement signals heading into 2026 point clearly toward intensified examinations by the OCC, FDIC, and SEC, with AI-enhanced monitoring tools enabling regulators to flag gaps in real time. Upcoming frameworks in the EU and US are expected to demand explainability for AI-driven AML decisions, requiring firms to prove why an algorithm flagged or did not flag a particular transaction.

Industry response has been decisive. Banks are forming strategic partnerships with RegTech vendors to automate the most resource-intensive compliance functions. Mastercard partnered with Trulioo to streamline KYC and AML checks for cross-border payment compliance, and Santander adopted ThetaRay’s AI-powered transaction monitoring platform to strengthen its AML capabilities. These are not experimental pilot programs. They are core operational investments.

The FCA is introducing new guidance effective September 2026 that will explicitly link non-financial misconduct, such as bullying and harassment, to fitness and propriety assessments. That expansion of what counts as a compliance failure underscores the trend toward broader, more holistic regulatory expectations that go well beyond traditional financial crime controls.

The institutions positioning themselves best for this environment share common characteristics. They invest in technology that automates routine compliance tasks while freeing skilled professionals to focus on judgment-intensive work. They treat regulatory change management as a standing capability rather than a project. They build compliance programs that scale as regulations evolve rather than requiring wholesale rebuilds every time a new rule takes effect.

Common Mistakes That Leave Banks Exposed

Even well-intentioned compliance programs fail when they fall into predictable traps. The most damaging mistakes in 2026 include relying on siloed systems that do not share data across business lines, leaving gaps that regulators can see even when internal teams cannot. Outdated policies that reference superseded rules create the impression of negligence even when the underlying controls are sound.

Ignoring jurisdictional disparities is another common failure. A policy that satisfies U.S. regulators may fall short of European or Asian requirements, and banks that treat compliance as a single global standard rather than a jurisdiction-by-jurisdiction obligation discover the gaps during exams rather than during planning.

Poor data quality quietly undermines everything else. When the underlying data feeding your risk assessments, transaction monitoring, and regulatory reports is incomplete or inaccurate, even the best technology and the most talented team will produce unreliable results. Boards and stakeholders who rely on those reports end up making decisions based on a distorted picture of reality.

Only 18% of AML professionals report having fully operational AI tools, which means that the vast majority of institutions are still running partially manual processes that cannot scale to meet the demands regulators are placing on them. Closing that gap is not optional. It is a competitive and regulatory survival requirement.

Looking Ahead: What 2026 and Beyond Will Demand

The trajectory is clear. Regulatory expectations are converging toward integrated global standards that demand real-time transparency, proactive risk management, and technology-driven compliance capabilities. Banks that embed these capabilities now will not just avoid penalties. They will operate more efficiently, make better decisions, and build the kind of regulatory trust that translates into competitive advantage.

The market for artificial intelligence in RegTech is forecast to reach $3.3 billion by 2026, growing at a compound annual growth rate of 36.1%. That investment reflects a collective bet by the industry that technology-led compliance is not a trend but the new baseline.

The financial institutions that will thrive amid ongoing regulatory whiplash are the ones that stop treating compliance as a cost center and start treating it as strategic infrastructure. They hire and train people who understand both the rules and the business. They invest in technology that scales with regulatory complexity rather than buckling under it. And they build cultures where compliance is everyone’s responsibility, not just the compliance department’s problem.

The rules will keep changing. That is not going to stop. The question is whether your institution is built to absorb the change or whether the next wave of regulatory whiplash will catch you flat-footed.

Frequently Asked Questions

What causes regulatory whiplash for banks in 2026?

Regulatory whiplash results from rapid policy shifts across multiple jurisdictions, overlapping and sometimes contradictory requirements from frameworks like MiFID II and GDPR, and escalating enforcement pressure driven by billions of dollars in fines for reporting failures and AML shortcomings. Political transitions, geopolitical tensions, and high-profile institutional failures all accelerate the pace of change, forcing banks to adapt continuously rather than on fixed cycles.

How can banks identify which regulations apply to them?

The most effective approach starts with building comprehensive regulatory inventories tailored to each business line, product type, and jurisdiction where the institution operates. Automated tools that monitor updates from bodies like the FCA, OCC, SEC, and FDIC help ensure that new obligations are flagged as soon as they are published. Without this kind of systematic tracking, banks risk discovering applicable rules only when a regulator points out the gap during an examination.

What role does technology play in beating regulatory whiplash?

RegTech automates the most resource-intensive compliance tasks, including risk assessments, policy enforcement, transaction monitoring, and regulatory reporting. AI-driven tools provide real-time alerts when rules change, flag suspicious activity with fewer false positives, and generate the documentation regulators expect during examinations. For context, the global RegTech market is on pace to nearly triple between 2023 and 2029, reflecting how central technology has become to compliance strategy across the industry.

Why is employee training essential for compliance?

Technology handles volume and speed, but compliance ultimately depends on human judgment. Employees need to understand the practical application of rules like BSA record-keeping requirements and AML duties so they can recognize red flags, make sound decisions in ambiguous situations, and defend their actions during audits. Training that is scenario-based, role-specific, and delivered in plain language produces far better results than generic annual certifications.

How do internal audits help financial institutions?

Routine audits serve as an early warning system, catching gaps and weaknesses before regulators find them. They also create the documented evidence of proactive risk management that institutions need during examinations. The key is closing the loop: identifying issues, assigning ownership for remediation, tracking progress, and verifying that fixes work. Auditing without follow-through creates a paper trail that actually works against you if regulators see unresolved findings.

Can smaller banks afford effective compliance programs?

Yes. The rise of RegTech-as-a-Service and cloud-based compliance platforms has made sophisticated automation accessible to community banks and mid-tier institutions that could never have built these capabilities in-house. Scalable SaaS solutions, vendor partnerships, and shared compliance resources allow smaller banks to meet the same regulatory standards as their larger competitors without matching their budgets.