Stablecoins are evolving into critical infrastructure for digital payments, and the GENIUS Act creates the first federal framework to govern them. So how does it work? Let me walk you through the best practices, detailed implementation steps, and how to measure success and drive continuous improvement.

Table of Contents

The GENIUS Act Scope

The GENIUS Act defines payment stablecoins as digital tokens redeemable one-to-one for U.S. dollars and removes them from SEC or CFTC jurisdiction. They must be backed by liquid reserves, adhere to consumer protections, and operate under a federal or certified state license. Start by reviewing the full text of the Act on Congress.gov.

Pull together legal, compliance, finance, technology, and risk teams. Assign executive sponsors responsible for monthly attestation, audit coordination, and board reporting. Create charters and meeting cadences to oversee each compliance pillar.

Reserve Management: Backbone of Trust

Identify Permissible Assets

Reserves can include U.S. currency, demand deposits at FDIC-insured banks, Treasury bills (maturities ≤93 days), and overnight repurchase agreements collateralized by Treasuries. Confirm eligibility by consulting the OCC’s charter guidelines.

Segregate and Track Reserves

- Step 1: Open dedicated reserve accounts at FDIC-insured institutions with no co-mingling of operational funds.

- Step 2: Implement a secure reconciliation system that matches on-chain token mint and burn events with off-chain reserve balances in real time.

- Step 3: Automate daily reporting dashboards to flag discrepancies immediately.

Attest and Audit

- Step 1: Engage independent auditors experienced in digital assets to perform quarterly attestations.

- Step 2: CEOs and CFOs certify monthly reserve reports under penalty of perjury.

- Step 3: Publish each attestation on a public transparency portal, linking to the auditor’s confirmation and financial statements.

Licensing Pathways: Choose Your Track

Federal OCC Charter

If you’re a nonbank entity, uninsured national bank, or foreign bank branch, apply for an OCC charter. So let me tell you what to do:

- Assemble a business plan outlining stablecoin use cases, governance models, and risk frameworks.

- Draft your capital and liquidity projections, stress-tested against redemption surges.

- Submit your application via the OCC’s application portal.

Certified State License

For issuers with less than $10 billion in circulation:

- Review your state banking regulator’s guidelines for stablecoin licensing.

- Confirm that your state’s rules are certified as “substantially similar” to federal standards by the Treasury’s review committee.

- File your application, including all consumer protection, privacy, and marketing policies.

Bank Subsidiary Route

FDIC-insured banks and NCUA credit unions operate via subsidiaries:

- Engage your primary federal regulator—FDIC, Federal Reserve, or NCUA—for supervisory expectations.

- Map your compliance controls to existing banking regulations and GENIUS Act requirements.

- Submit your charter amendment or subsidiary license application.

Building a Robust Compliance Program

AML/KYC Framework

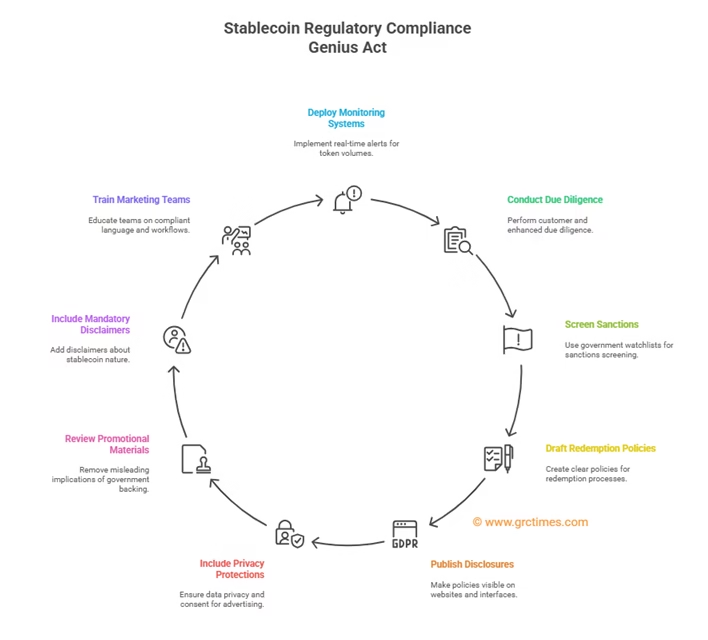

- Step 1: Deploy transaction-monitoring systems tailored for token volumes, with real-time alerts.

- Step 2: Implement customer due diligence and enhanced due diligence for high-risk clients.

- Step 3: Conduct ongoing sanctions screenings using government watchlists.

Consumer Disclosures

- Step 1: Draft clear redemption policies, outlining processes, fees, and timelines.

- Step 2: Publish these disclosures prominently on your website and in wallet interfaces.

- Step 3: Include privacy protections, specifying that transaction data won’t be used for targeted advertising without consent.

Marketing Controls

- Step 1: Review all promotional materials to remove any implication of government backing or FDIC insurance.

- Step 2: Include mandatory disclaimers: “Stablecoins are private-sector obligations, not legal tender.”

- Step 3: Train marketing teams on compliant language and approval workflows.

Technology & Infrastructure

Secure Custody Architecture

- Step 1: Implement multi-signature wallets that separate hot and cold storage.

- Step 2: Restrict access with hardware security modules (HSMs) and multi-factor authentication.

- Step 3: Monitor on-chain flows with blockchain analytics tools to detect anomalies.

Redemption Platform

- Step 1: Build scalable APIs and user interfaces that can handle redemption spikes seamlessly.

- Step 2: Integrate fraud-prevention checks to balance speed with security.

- Step 3: Automate notifications to users and internal teams about redemption status.

Transparency Dashboard

- Step 1: Develop a public dashboard displaying real-time token supply, reserve breakdowns, and audit attestations.

- Step 2: Embed links to audit reports and regulator filings.

- Step 3: Update data continuously and verify accuracy through automated data pipelines.

Regulatory Engagement & Reporting

Proactive Outreach

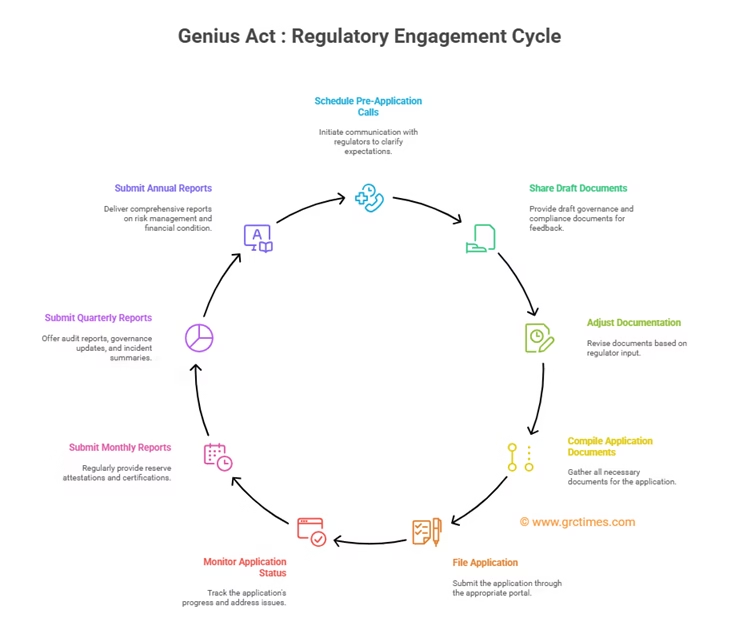

- Step 1: Schedule pre-application calls or meetings with the OCC, FDIC, or state regulator to clarify expectations.

- Step 2: Share draft governance charters and compliance frameworks for early feedback.

- Step 3: Adjust your documentation based on regulator input before final submission.

Licensing Application

- Step 1: Compile governance documents, business plans, capital and liquidity models, audit plans, and compliance programs.

- Step 2: File through the appropriate portal (OCC, state banking department, or primary federal regulator).

- Step 3: Monitor application status and promptly address any deficiency letters.

Ongoing Reporting

- Monthly: Submit reserve attestations and CEO/CFO certifications via your transparency portal.

- Quarterly: Provide audit reports, governance updates, and incident summaries.

- Annual: Deliver comprehensive reports on risk management, financial condition, and remediation progress.

Measuring Success & Continuous Improvement

Define Key Metrics

- Redemption Processing Time: Measure average and peak processing duration to identify bottlenecks.

- Audit Compliance Rate: Track on-time completion of auditor attestations and regulatory filings.

- Consumer Satisfaction: Survey users on clarity of disclosures, redemption experience, and support responsiveness.

- Regulatory Findings: Monitor the number and severity of examination exceptions or enforcement actions.

Conduct Regular Reviews

- Quarterly Self-Assessments: Compare internal controls against GENIUS Act requirements and regulator guidance.

- Incident Post-Mortems: After any redemption delays or system outages, analyze root causes, update playbooks, and communicate lessons learned.

- Policy Refresh Cycles: Review and update all policies—AML/KYC, consumer disclosures, marketing controls—biannually or in response to significant rule changes.

Industry Collaboration

- Join working groups and consortia to share best practices, co-develop standards, and provide unified feedback to regulators.

- Participate in conferences and webinars hosted by the Federal Reserve, OCC, or state banking associations.

Staying Ahead of Regulatory Changes

- Subscribe to regulator newsletters and rulemaking dockets from the OCC, FDIC, Federal Reserve, FinCEN, and CFPB.

- Monitor bills and guidance from Congress and the Treasury’s review committee, adapting your compliance roadmap in advance of formal rules.

By following these best practices and detailed steps, organizations can not only achieve compliance with the GENIUS Act but also build a sustainable, transparent, and consumer-friendly stablecoin service that thrives under federal oversight.

FAQ

What key steps should I take first?

Begin with a detailed gap analysis, assemble your governance committee, and choose the optimal charter pathway—OCC charter, certified state license, or bank subsidiary.

How frequently must we attest reserves?

Monthly CEO/CFO certifications and quarterly third-party audits are required, with all reports publicly posted.

Can interest-bearing reserves ever be allowed?

No. The GENIUS Act explicitly prohibits paying interest on reserve assets to ensure full liquidity and backing.

What happens if reserve levels fall below requirements?

Issuers must notify regulators immediately, suspend redemptions if necessary, and deploy contingency liquidity lines to restore adequacy.

How do we ensure consumer privacy?

Implement strict data-use policies, prohibiting the sale or use of transaction data for targeted advertising without explicit customer consent.

What is the transition period for existing stablecoins?

Non-compliant offerings must wind down by July 18, 2028. Plan to migrate or redeem holders before that deadline.